When most entrepreneurs think of patents, their minds typically go to "Defensibility"—protecting their innovations from competitors. Some might also consider "Diligence," as patents are often a positive signal for investors in a data room.

However, there's another crucial "D word" that might come as a surprise: Dilution.

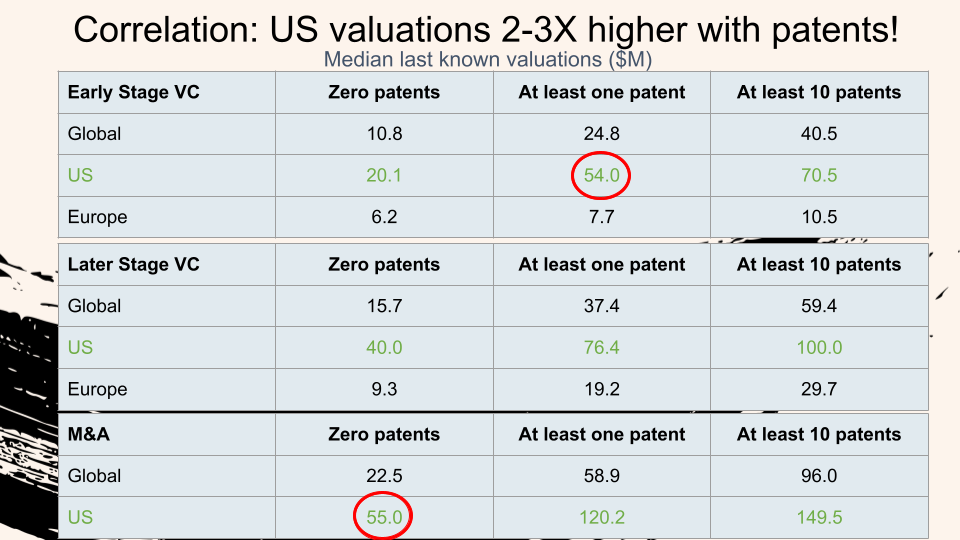

There’s a significant, positive correlation between a startup's patent count and its post-money valuation, directly impacting how much equity founders retain in future funding rounds.

Using data from Pitchbook on climate tech and cleantech startups, my analysis tested for any correlation between valuations at various venture investment stages (Seed, Accelerator/Incubator, Early Stage VC, and Later Stage VC) and the number of active and pending patents, and it revealed some compelling findings.

The implication for dilution is profound: a higher valuation means you surrender less equity for the same amount of investment, effectively preserving more of your ownership stake. As a former corporate attorney used to frequently remind me when negotiating a financing round, "it’s all about dilution."

My analysis identifies a correlation, not causation—other factors certainly contribute to valuation differences, and this is why I wanted to include a question mark in the title of this post; we have found no smoking gun. Still, the statistical significance of these findings is strong. The differences in median post-money valuations are statistically significant, with p-values ranging from 10^-4 to 10^-16.

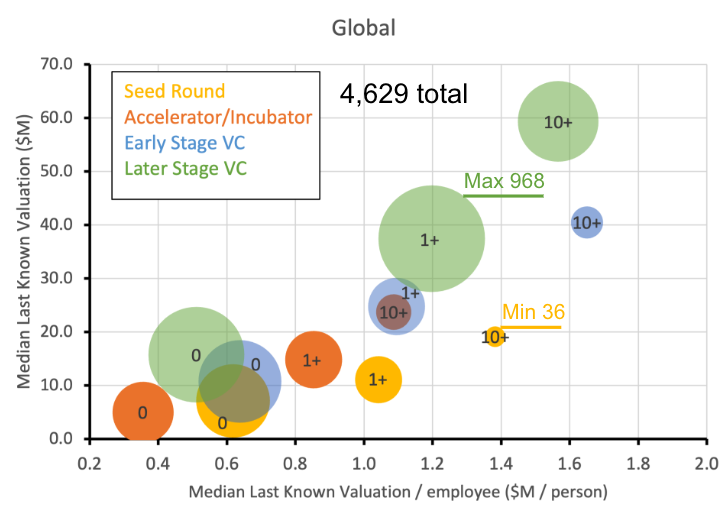

Furthermore, positive correlations with patents remained strong even after normalizing valuations by the number of employees, suggesting a robustness to this trend across different company sizes (Figure 2).

The distributions of deal dates for companies with and without patents are indistinguishable 1, indicating that the valuation differences are not merely a matter of timing. And in terms of company ages, early startups with patents tend to be older (median age +1 year for Seed and Early Stage VC, +3 years for Accelerator/Incubator). Notably, startups with patents tend to be older, especially at Seed, Accelerator/Incubator, and Early Stage VC rounds. Pitchbook reports an empty entry to identify companies with no (zero) active and pending patents, and the zero patent count was tested for US companies across all stages using Patsnap, which resulted in a 6-12% correction rate. Licensed patents not assigned to the startup were not quantified also.

For early-stage deep tech companies, the idea of "10+ active and pending patents" might seem like a lot of inventions and expensive. But keep in mind, one key innovation captured within a single patent family can easily generate this number when considering international filings across multiple countries and divisional applications. Moreover, using ~$500k is an estimate for the cost of 10 patents over their 20-year life space, the positive correlation strength on valuations at later stages suggests the ROI is more than worth the financial and time commitment.

My analysis filtered for companies within climate tech and clean tech verticals to ensure accurate comparisons. While the specific numbers relate to these sectors, the underlying principle suggests a broader applicability for industries where intellectual property is a core asset.

Ultimately, investing in patents is not just about legal protection; it's a strategic move for value creation. The next time you devise your intellectual property strategy, remember the "Dilution" factor. Your patent portfolio isn't just a shield against competitors; it could be a powerful lever for enhancing your startup's valuation and safeguarding your hard-earned equity.

1/ Mood’s median test for two samples (with and without patents) used to determine whether the medians of two independent samples are equal (the null hypothesis). Uses a chi-square test of independence. Refs: https://real-statistics.com/non-parametric-tests/moods-median-test-two-samples/

https://toptipbio.com/chi-square-test-independence-excel/

2/ Pitchbook classifies a deal as Seed using Form D data, and accelerator/Incubator refers to an event in which a company joins a program that variably provides funding, office space, technological development and/or mentorship, often in exchange for equity in the company.