The energy transition has never been more metal-intensive. Copper wire carries clean electricity across continents; aluminum sheaths solar modules and wind turbines; lithium, cobalt, nickel, and rare earths anchor every battery powering the green economy. But the supply chains behind these metals remain dangerously linear. We dig, refine, use, and discard – leaving billions in materials stranded in landfills, factories, and forgotten scrap yards.

Metal recycling offers an alternative. Done right, it can deliver virgin-grade metals without the emissions, permitting delays, or geopolitical risks of mining.

Yet, today’s system isn’t up to the task. End-of-life (EoL) recycling rates are dismal. Traceability is spotty. Downcycling is the norm. As a result, fewer than 40% of essential transition metals are ever truly recovered – a $60 billion opportunity hiding in plain sight.

The global metals recycling system fails where it matters most: quality.

Built for volume over value, today’s infrastructure maximizes throughput while sacrificing material integrity. Metals from electronics, vehicles, and industrial components are lumped together, shredded, and melted – destroying alloy structures and producing low-grade, contaminated outputs. The result is a system that recovers metals, but not their function. These downcycled materials are sold at a discount, often unable to meet the purity or performance standards required for high-spec applications like EV drivetrains, batteries, or aerospace components – effectively locking them out of the very industries driving demand for critical materials.

In technical terms: Effective recycling = EoL recovery × (1 – Downcycling rate).

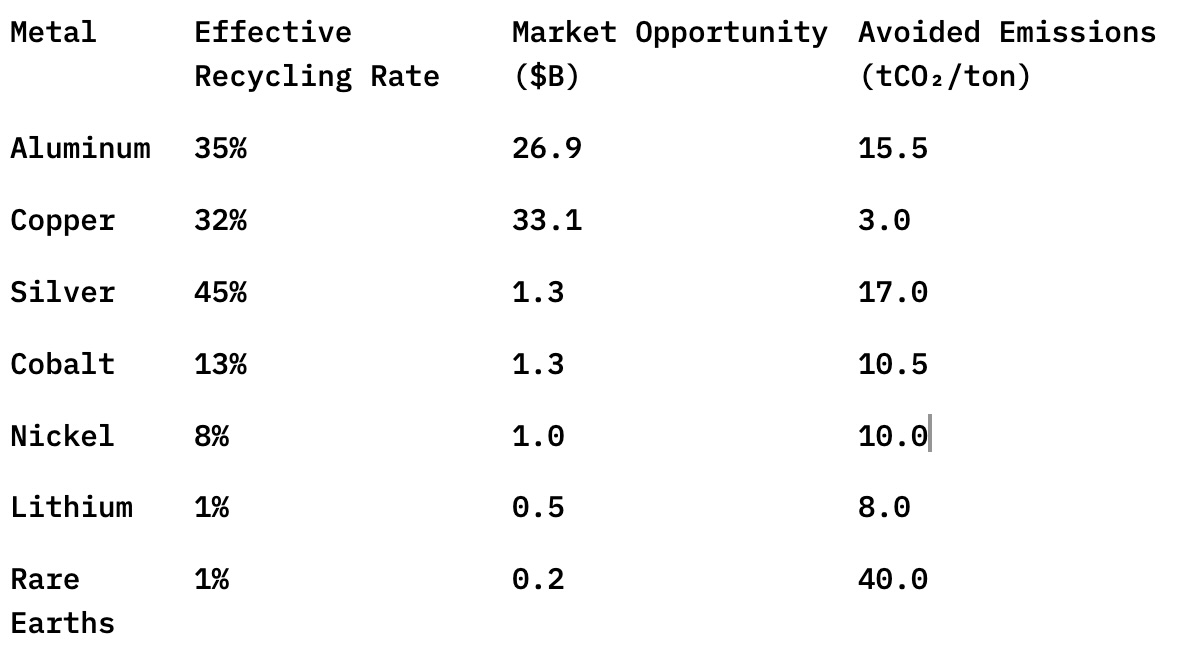

That second factor – loss of purity and performance – is where most value erodes. Take aluminum: while 70% of end-of-life aluminum is collected, only about half maintains the purity needed to replace virgin metal, bringing the effective recycling rate down to just 35%. Copper performs even worse, with complex assemblies like motors and wires dragging rates to around 32%. For lithium and rare earth elements, the numbers are stark – effective recycling hovers near 1%, barely registering on the global materials balance.

This is not a technological inevitability – it’s a system design failure.

Three forces have aligned to make metal recycling a critical leverage point:

1. Flight to Quality. Original Equipment Manufacturers (OEMs) – especially in batteries, aerospace, and clean energy – require high-purity, spec-compliant materials. Most recycled feedstock today cannot meet these specs, limiting reuse and keeping manufacturers tied to virgin supply (mining).

2. Regulatory Tailwinds. Europe’s battery directive and U.S. domestic content requirements are turning recycled content from a nice-to-have into a compliance mandate. Companies that can verify the origin, composition, and performance of recycled metals will be first in line for procurement contracts.

3. Surging EoL Volumes. The first wave of EVs, solar panels, and consumer electronics is reaching end-of-life, creating a fast-growing stream of valuable waste. Black mass – the crushed material left after battery dismantling – is rich in lithium, nickel, cobalt, and graphite. But recovering it at spec requires selective chemistry, not brute force.

Recycling isn’t just cleaner. It’s faster, cheaper, and often more politically tractable than mining. It can unlock circular economies across multiple material classes – but only if we build systems designed for spec, not scrap.

Opportunities in metal recycling map cleanly to three failure points: (1) loss of purity, (2) complexity of recovery, and (3) lack of traceability. Compounding these challenges, the value of feedstock scrap metal is highly volatile, shaped by global commodity swings that can undercut the economics of recycling. In response, a new generation of companies is redesigning systems around purity and performance – not just recovery volume – to ensure more consistent value capture.

Metal quality degradation is widespread, stemming from complex contamination sources such as paint residues, surface coatings, alloy blending, and sorting inefficiencies. This is particularly acute for aluminum, where slight deviations in composition prevent reuse in high-performance applications like aircraft or automotive parts. In nickel, most recovered material is low-grade Class II, unsuitable for batteries that require high-purity Class I. In copper, contamination from mixed wires and oxidation lowers purity, restricting recycled copper to lower-value uses instead of electronics or EVs.

Startups are tackling these challenges with advanced solutions: AI-driven sorting, precise alloy recognition, melt analysis, and selective refining – all designed to restore quality at the pre-treatment stage. Beyond recovery, some startups are enabling spec upgrades post-recovery, converting low-grade feedstock into battery-grade or electronics-ready metals. Leading companies combine novel material technologies with modular, drop-in systems that replace traditional smelters and acid-leaching with compact, ambient-temperature processes – delivering high-spec metals without the emissions or downtime.

Even when feedstock is available, recovery often falters due to technical challenges. Black mass contains valuable metals but in chemically complex forms that strain conventional hydrometallurgy. Silver and platinum group metals (PGMs) occur in trace amounts across solar panels, circuit boards, and catalytic converters, demanding high-precision, low-volume recovery systems.

Emerging technologies are rising to meet this challenge. Modular hydrometallurgy platforms, robotic disassembly systems, and tunable separation chemistries enable more selective, spec-grade recovery with reduced energy and reagent use. Some solutions are gaining early traction by efficiently extracting high-value metals from acid-rich, multi-contaminant streams – providing a viable alternative to traditional smelting and precipitation methods.

Even when recycled metals meet technical standards, the lack of verifiable data limits offtake. Manufacturers – particularly in automotive, electronics, and defense sectors – demand documented performance and provenance before incorporating recycled metals into their supply chains.

Material passports, digital twins, and real-time quality assurance systems are beginning to address this gap. By pairing physical recovery with chemical analysis and digital traceability, startups can close the loop – ensuring that recycled metals are not just technically sound, but contractually and reputationally reliable.

The most differentiated players embed traceability into their process architecture itself – generating real-time purity data, linking quality assurance metrics to offtake agreements, and enabling unprecedented supply chain confidence. This capability is no longer optional; it’s rapidly becoming a procurement mandate.

Not all metals are created equal when it comes to recycling opportunities. The most investable targets combine (1) large volumes, (2) high downcycling risk, and (3) emissions-intensive virgin supply chains:

Aluminum and copper offer the largest absolute impact due to scale and avoided emissions. Rare earths, lithium, and cobalt, though smaller in market size, offer asymmetric upside: they are high-cost, high-risk materials where even modest recycling improvements can dramatically increase supply resilience.

As with mining, the toughest challenge in metal recycling isn’t technology – it’s value capture. Today’s scrap yards and recyclers operate on razor-thin margins, while OEMs demand high-spec inputs. The companies positioned to thrive will be those that bridge that gap.

Three main archetypes are emerging:

1. Full-Stack Refiners. These companies manage the entire value chain – from feedstock collection to refining and quality assurance. By integrating upstream and downstream operations, they maintain control over purity, guarantee traceability, and secure direct offtake agreements. While capital-intensive, this model offers strong, defensible long-term economics.

2. Upstream Enablers. Focused on sorting, diagnostics, and disassembly, these startups provide critical tools to existing recyclers, boosting throughput and yield. Their models often rely on equipment sales or licensing, enabling faster market entry but with thinner margins.

3. Traceability-as-a-Service. These companies don’t touch the metal at all. Instead, they provide digital IDs, real-time analytics, and chain-of-custody platforms that reduce risk for industrial buyers integrating recycled materials.

Each approach involves trade-offs: full-stack refiners command higher margins but require significant capital; enablers and traceability services move faster but depend heavily on partnerships and integration. As regulations and buyer demands evolve, hybrid models are likely to emerge.

The metals required for the energy transition are already here: embedded in the products we’ve used, the factories we’ve built, and the waste we’ve overlooked. The challenge isn’t scarcity – it’s recovery. And the solutions aren’t speculative – they’re commercial.

For founders and investors, the playbook is clear:

We are in the early stages of a new supply chain – one built not on extraction, but on precision recovery. In that shift emerges a new class of industrial infrastructure: clean, modular, chemistry-driven systems that make circularity not just possible, but profitable. Mining built the industrial world. But to sustain the next one, we’ll need to recycle it.