When the Inflation Reduction Act (IRA) passed in 2022, it promised a decade-long runway of clean energy investment incentives. Three years later, that promise has been cut short. While the Trump administration and Congress have not repealed the IRA outright they have significantly narrowed its scope. Through executive orders, budget rescissions, and July’s “One Big Beautiful Bill,” many of the law’s most visible tax credits have been phased out early. As predicted, consumer-facing renewable incentives have borne the brunt of the cuts, while manufacturing, nuclear, and energy security provisions have largely endured. The difference between our initial analysis and the reality that has played out is one of scale: rollbacks have gone further and faster than many anticipated.

The administration’s declaration of a National Energy Emergency and its “Unleashing American Energy” executive order have delivered sweeping deregulation, fast-tracking oil, gas, nuclear, and mining permits. While we anticipated this tilt, the pace has been faster than forecast. Nuclear and geothermal have been clear winners, with advanced nuclear startups like Oklo and TerraPower advancing approvals at record pace. Solar leaders such as Sunrun and Enphase, by contrast, face headwinds from new tariffs on Chinese panels. Meanwhile, mining companies are also riding this wave of deregulation, with KoBold Metals securing over $500 million this year to expand its AI-driven copper and nickel exploration portfolio across the U.S. and Africa.

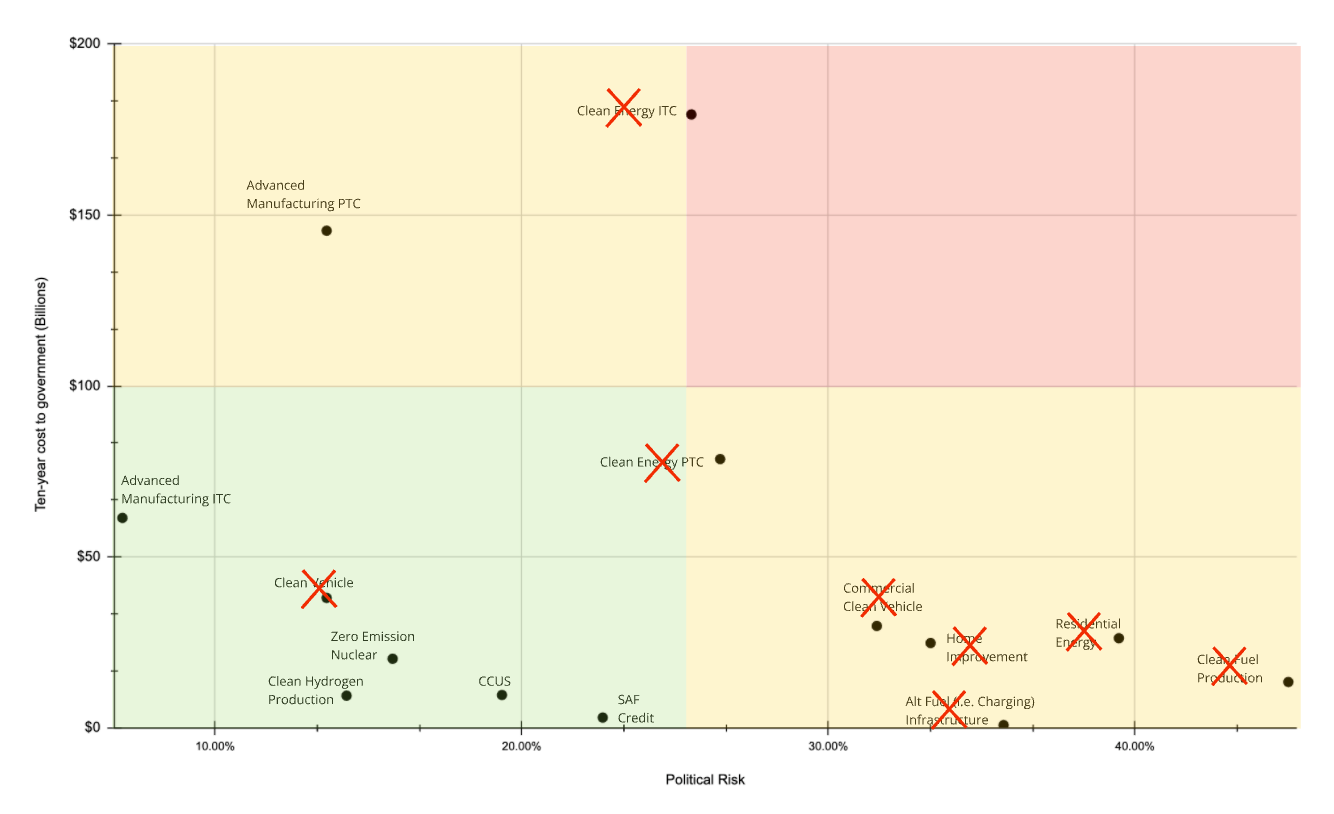

We wrote that a full repeal was unlikely but reallocations were probable. That has now played out. The July 2025 reconciliation package — the so-called One Big Beautiful Bill — rescinded unobligated IRA funds and accelerated the phaseout of major credits.

By the end of 2025, EV, residential energy, and home improvement credits will vanish. The Clean Energy ITC/PTC, which once accounted for ~40% of IRA spending, will apply only to projects breaking ground by 2026 and online by 2027. Still, manufacturing, nuclear, and hydrogen credits have survived, confirming our thesis that programs tied to energy security and reshoring would endure.

Our 2025 outlook highlighted the bipartisan Manchin–Barrasso permitting reform bill. While the bill continues to inch through Congress, its impact has already been effectively achieved by executive order. Trump’s energy directive has already delivered expedited approvals for LNG, grid projects, and mining. LNG exporters like Cheniere Energy have been among the biggest beneficiaries, moving forward at unprecedented speed. Renewable developers, by contrast, see only modest relief: Pattern Energy, for example, faces fewer transmission backlogs but remains hemmed in by weakening federal incentives.

Tariffs on Chinese minerals and components are accelerating investment into domestic refining and processing. Automakers such as Ford and Volkswagen now face the dual challenge of shrinking consumer EV credits and mounting pressure to localize their supply chains. In this reshoring race, startups providing enabling technologies are emerging as clear winners. At One Ventures’ latest investment, ChemFinity, exemplifies this shift—its polymeric sorbent platform delivers high-purity metal recovery that aligns directly with U.S. and European security priorities. While consumer-side demand softens, defense and national security imperatives are anchoring long-term capital flows into domestic supply chains.

Our call of uneven support has proven true: traditional ethanol producers like POET, backed by entrenched agricultural lobbying, continue to enjoy protection, while advanced biofuels and e-fuels face subsidy erosion. CCUS projects remain intact, but face funding gaps as DOE grants shrink and consolidation pressure mounts.

Broad industrial decarbonization has slowed, but selective opportunities persist where technologies intersect with industrial policy. Companies positioning themselves as enablers of U.S. competitiveness and jobs are still raising significant capital. Boston Metal in the U.S. and H2 Green Steel in Sweden are leading examples, driving forward steel decarbonization.

Our original thesis — that success in this environment depends on technologies rooted in durable physics and financial fundamentals rather than fleeting incentives — is playing out. The IRA has shifted from an era of expansion to contraction. Federal support remains, but it is narrower, shorter-term, and increasingly shifting toward nuclear, reshoring, fossil-adjacent infrastructure. Renewables and consumer-facing incentives will continue to face headwinds,while companies positioned as critical to energy security and industrial competitiveness are emerging as enduring winners. Clean tech developers and investors must now navigate a less predictable federal landscape, with state-level policy and global markets playing a larger role.